Thank you all for reading this blog, which I have now moved to the Substack platform, where I am making weekly posts -- two so far.

You can subscribe free at https://jimsmith145.substack.com/

See you there!

Thank you all for reading this blog, which I have now moved to the Substack platform, where I am making weekly posts -- two so far.

You can subscribe free at https://jimsmith145.substack.com/

See you there!

July 17, 2023

A story

in the New York Times

today by Jonathan Swan, Charlie Savage, and Maggie Haberman outlined how

former president Donald Trump and his allies are planning to create a

dictatorship if voters return him to power in 2024. The article talks about

how Trump and his loyalists plan to “centralize more power in the Oval

Office” by “increasing the president’s authority over every part of the

federal government that now operates, by either law or tradition, with any

measure of independence from political interference by the White House.” They

plan to take control over independent government agencies and get rid of the

nonpartisan civil service, purging all but Trump loyalists from the U.S.

intelligence agencies, the State Department, and the Defense Department. They

plan to start “impounding funds,” that is, ignoring programs Congress has

funded if those programs aren’t in line with Trump’s policies. “What

we’re trying to do is identify the pockets of independence and seize them,”

said Russell T. Vought, who ran Trump’s Office of Management and Budget and

who now advises the right-wing House Freedom Caucus. They envision a

“president” who cannot be checked by the Congress or the courts. Trump’s

desire to grab the mechanics of our government and become a dictator is not

new; both scholars and journalists have called it out since the early years

of his administration. What is new here is the willingness of so-called

establishment Republicans to support this authoritarian power grab. Behind

this initiative is “Project 2025,” a coalition of more than 65 right-wing

organizations putting in place personnel and policies to recommend not just

to Trump, but to any Republican who may win in 2024. Project 2025 is led by

the Heritage Foundation, once considered a conservative think tank, that

helped to lead the Reagan revolution. A piece

by Alexander Bolton in The

Hill today said that Republican senators are “worried” by the

MAGAs, but they have been notably silent in public at a time when every

elected leader should be speaking out against this plot. Their silence

suggests they are on board with it, as Trump apparently hoped to

establish. The

party appears to have fully embraced the antidemocratic ideology advanced by

authoritarian leaders like Russia’s president Vladimir Putin and Hungary’s

prime minister Viktor Orbán, who argue that the post–World War II era, in

which democracy seemed to triumph, is over. They claim that the tenets of

democracy—equality before the law, free speech, academic freedom, a

market-based economy, immigration, and so on—weaken a nation by destroying a

“traditional” society based in patriarchy and Christianity. Instead

of democracy, they have called for “illiberal” or “Christian” democracy,

which uses the government to enforce their beliefs in a Christian,

patriarchal order. What that looks like has a clear blueprint in the actions

of Florida governor Ron DeSantis, who has gathered extraordinary power into

his own hands in the state and used that power to mirror Orbán’s destruction

of democracy. DeSantis

has pushed through laws that ban abortion after six weeks, before most people

know they’re pregnant; banned classroom instruction on sexual orientation and

gender identity (the “Don’t Say Gay” law); prevented recognition of

transgender individuals; made it easier to sentence someone to death; allowed

people to carry guns without training or permits; banned colleges and

businesses from conversations about race; exerted control over state

universities; made it harder for his opponents to vote, and tried to punish

Disney World for speaking out against the Don’t Say Gay law. After rounding

up migrants and sending them to other states, DeSantis recently has called

for using “deadly force” on migrants crossing unlawfully. Because

all the institutions of our democracy are designed to support the tenets of

democracy, right-wingers claim those institutions are weaponized against

them. House Republicans are running hearings designed to prove that the

Federal Bureau of Investigation and the Department of Justice are both

“weaponized” against Republicans. It doesn’t matter that they don’t seem to

have any evidence of bias: the very fact that those institutions support

democracy mean they support a system that right-wing Republicans see as

hostile. “Our

current executive branch,” Trump loyalist John McEntee, who is in charge of

planning to pack the government with Trump loyalists, told the New York Times

reporters, “was conceived of by liberals for the purpose of promulgating

liberal policies. There is no way to make the existing structure function in

a conservative manner. It’s not enough to get the personnel right. What’s

necessary is a complete system overhaul.” It has

taken decades for the modern-day Republican Party to get to a place where it

rejects democracy. The roots of that rejection lie all the way back in the

1930s, when Democrats under Franklin Delano Roosevelt embraced a government

that regulated business, provided a basic social safety net, and promoted

infrastructure. That system ushered in a period from 1933 to 1981 that

economists call the “Great Compression,” when disparities of income and

wealth were significantly reduced, especially after the government also began

to protect civil rights. Members

of both parties embraced this modern government in this period, and Americans

still like what it accomplished. But businessmen who hated regulation joined

with racists who hated federal protection of civil rights and traditionalists

who opposed women’s rights and set out to destroy that government. In West

Palm Beach, Florida, last weekend, at the Turning Points Action Conference,

Representative Marjorie Taylor Greene (R-GA) compared President Biden’s Build

Back Better plan to President Lyndon Baines Johnson’s Great Society programs,

which invested in “education, medical care, urban problems, rural poverty,

transportation, Medicare, Medicaid, food stamps, and welfare, the Office of

Economic Opportunity, and big labor and labor unions.” She noted that under

Biden, the U.S. has made “the largest public investment in social

infrastructure and environmental programs, that is actually finishing what

FDR started, that LBJ expanded on, and Joe Biden is attempting to

complete.” Well,

yeah. Greene

incorrectly called this program “socialism,” which in fact means government

ownership of production, as opposed to the government’s provision of benefits

people cannot provide individually, a concept first put into practice in the

United States by Abraham Lincoln and later expanded by leadership in both

parties. The administration has stood firmly behind the idea—shared by LBJ

and FDR, and also by Republicans Lincoln, Theodore Roosevelt, and Dwight

Eisenhower, among others—that investing in programs that enable working

people to prosper is the best way to strengthen the economy. Certainly,

Greene’s speech didn’t seem to be the “gotcha” that she apparently hoped. A

March 2023 poll by independent health policy pollster KFF, for example, found

that 80% of Americans like Social Security, 81% like Medicare, and 76% like

Medicaid, a large majority of members of all political parties. The

White House Twitter account retweeted a clip of Greene’s speech, writing:

“Caught us. President Biden is working to make life easier for hardworking

families.” — Notes: https://www.nytimes.com/2023/07/17/us/politics/trump-plans-2025.html https://www.washingtonpost.com/politics/2023/06/07/house-republicans-mccarthy-russell-vought-trump/ https://www.nytimes.com/2023/06/26/us/politics/ron-desantis-border-drug-traffickers.html https://twitter.com/Acyn/status/1680582110636064768 https://twitter.com/WhiteHouse/status/1680940415812354049 https://thehill.com/homenews/senate/4098609-gop-senators-rattled-by-radical-conservative-populism/

© 2023 Heather Cox Richardson |

Here's the excerpt from Thom's email newsletter today:

None of the states suing would have suffered any harm from the loan forgiveness, because they were federal loans. There literally was “no injury” to any of the parties bringing the lawsuit, meaning they had no legal standing to be in court. The company (MOHELA) John Roberts cited in his bizarre, deceitful, and nakedly lying opinion also suffered no loss and explicitly asked not to even be listed as a party to the case, although the Republicans on the Court insisted on keeping them in to provide a fig leaf.

For a case to be presented and litigated before a court — particularly the Supreme Court — there must be an injured party. Without that injured party there is no “standing” to sue and the case is typically thrown out. [Emphasis added] Even though MOHELA suffered NO injury here — it was a state-based lender that did not participate in federal student loans and thus did not lose a penny — Roberts weaseled them into the case just so he and his five Republican buddies could screw America’s student borrowers to satisfy the billionaires who put them on the Court and help maintain their lavish vacations and lifestyles.

I’m writing this column in the immediate aftermath of attending the Colorado Environmental Film Festival. I was only able to watch 20 or so of the 90-plus films featured during the sixteen 2-hour sessions, but I plan to watch others this week. (You can access all the films at www.CEFF.net for $75, which gives you seven days to view any collection you log into by Sunday, March 5.)

My favorite films were: The Sacrifice Zone; Wings over Water; Heart of Maui; Somehow Hopeful; Earth Girl; The Witness Is a Whale; and A Rally for Rangers.

Many of these films raised my consciousness regarding different issues facing humanity and America, which got me thinking about the term “Woke,” which is applied negatively against those of us with similar awareness of certain issues. In the parlance of the MAGA folks, I’m part of the “Woke mob.”

Obviously, the term is adapted from “awake” or “awakened.” One thing for which we can thank the previous administration is that the division it spawned awakened people like me to portions of our history (and our present) of which we may have been less aware. I’m thinking of books like The 1619 Project and Caste, which taught me things I did not know about our nation’s sad legacy of enslavement and racism, which are at the heart of America’s “great experiment.” For example, I didn’t realize that the 13th amendment abolished slavery, “except as a punishment for crime whereof the party shall have been duly convicted,” an exception that was exploited throughout the former confederate states by convicting Blacks of petty or false crimes and imprisoning them so that the prisons could lease them to plantation owners to continue their enslavement.

Yes, I’m awake to many aspects of our history to which the MAGA mob is (and would like to remain) unconscious. I’m awake to the environmental injustice suffered by the minority communities close to the Suncor plant in north Denver, which was the topic of a CEFF film. I’m awake to the broken promise of “40 Acres and a Mule” which underlies the calls for reparations to descendants of the enslaved.

I prefer “woke” to “unconscious.”

![]()

With

Ron DeSantis, we may finally be facing an all-American politician who has

Mussolini’s guile, ruthlessness, and willingness to see people die to advance

his political career

Rosaline is a 60-year-old Floridian who hopes

she doesn’t get seriously ill because she’d be wiped out by the increase in her

already burdensome medical debt. She has no insurance, and won’t qualify for

Medicare for another 5 years. Ron DeSantis is just fine with this. Cruelty is his trademark. During the

pandemic, Congress appropriated billions to help states expand their Medicaid

programs. That money is coming to an end this year, meaning Florida — which

refused to expand Medicaid with the federal subsides offered by the Affordable

Care Act — is set to throw another 2 million or so residents off their only

possible source of health insurance. Still, Ron

DeSantis refuses to expand Medicaid, even though 93 percent of the cost is covered with money from Washington, DC. It’s

the principle of the thing, apparently: he’s one of 11 red state governors who

believes that working poor people simply shouldn’t get health coverage. After

all, they didn’t have the good sense to be born into a wealthy family! Michael, 30, lives in Orlando and has asthma,

but running his little business buying and selling used furniture hasn’t earned

him enough to cover his medical bills and to pay rent. He recently got an

eviction notice, telling the Florida

Health Justice Project: “I was

given a list of homeless shelters to choose from but I hope it doesn’t come to

that.” Ron DeSantis is just fine with this. Cruelty is his trademark. Violence,

hate, bigotry, and cruelty are the four cardinal points of fascism. Compassion

and concern for the greater good, for the poor and weak, for the victims of

fate and accident have no place in the fascist world. Historians

and political observers have been predicting that America would get our very

own Mussolini ever since the days of Barry Goldwater. And there’s been no

shortage of candidates: bribe-taking Nixon; Central American fascist-loving

Reagan; Gitmo torturing and war-lying Bush; and, of course, Trump. But with Ron DeSantis, we may finally be facing an all-American

politician who has Mussolini’s guile, ruthlessness, and willingness to see

people die to advance his political career, all while being smart and educated

enough to avoid the easily satirized buffoonishness of Trump. Mussolini

was a famously short man who strutted with his muscular chest pushed out and

his chin jutted forward, just like DeSantis, who Trump says is musclebound, likes to do. Both men

were socially awkward, craved power, lacked empathy, displayed casual cruelty, sucked up to the wealthiest men in the nation, and

demonized opposition politicians — literally calling or implying their fellow

citizens are “the enemy” (a favorite trick of Hitler and Orbán, as well) — to

encourage their followers to support them or entertain the rhetoric of violence

and threats of violence to achieve political ends. Miriam, a single parent of two young children,

discovered a lump in her breast but postponed visiting the doctor for months

because she had no health insurance with her job as a housekeeper. Finally,

she realized the potential gravity of her situation. “I

needed to live to be there for my children,” she said. She got

treatment through the charity ward of a hospital, but even that treatment came

with a cost of $2,183. She slipped behind in the $200 monthly payments when her

job vanished with the pandemic and now she’s struggling to pay the $1783 she

still owes in co-payments from her treatments. She’s been sent to collection

and is living in fear of what’s next when the court finally comes after her. Ron DeSantis is just fine with this. Cruelty is his trademark. George

Washington, in his Farewell Address, warned us of the possible rise of

politicians like DeSantis who would suggest other Americans are enemies of the

nation’s values, who would exaggerate policy differences in war-like terms, and

who would ascribe the most evil of motives and intentions to simple political

opponents. “The

alternate domination of one faction over another, sharpened by the spirit of

revenge, natural to party dissension, which in different ages and countries has

perpetrated the most horrid enormities, is itself a frightful despotism.” But it

wasn’t just that calling other politicians enemies or attributing evil

motivations to them produced dissension and could tear a society apart,

although those concerns were at the top of Washington’s mind. He also knew that such rhetoric was the platform from which a

literal strongman could arise in America, destroying the democracy he’d fought

the Revolutionary War to create: “But

this leads at length to a more formal and permanent despotism,” he told the

nation. “The disorders and miseries which result gradually incline the minds of

men to seek security and repose in the absolute power of an individual; and

sooner or later the chief of some prevailing faction, more able or more

fortunate than his competitors, turns this disposition to the purposes of his

own elevation, on the ruins of public liberty.” Such a

warlike approach to politics, Washington said, could only lead in one

direction: “It

agitates the community with ill-founded jealousies and false alarms, kindles

the animosity of one part against another, foments occasionally riot and

insurrection.” Such

rhetoric, Washington argued, produces: “A fire

not to be quenched, it demands a uniform vigilance to prevent its bursting into

a flame, lest, instead of warming, it should consume.” It’s been

225 years since George Washington uttered those words. And now we’re here. Hipolito, the father of four, is worried about

his life’s partner, the mother of their children. “My

wife has been in pain for weeks now but we can’t afford to find out why,”

Hipolito told the Florida

Health Justice Project. “I swear, I’m very afraid. She is pale and

suffering every day.” He notes

that his wife hasn’t visited the doctor because their family can’t afford the

expense when they must also house, feed, and clothe their kids on his job as a

cook. Ron DeSantis is just fine with this. Cruelty is his trademark. Arresting

black men for voting, terrifying them and ruining their lives while making sure

they all get paraded in chains before the cameras. Threatening

public school teachers with prison for simply teaching history. Lying

about medical science regarding vaccines to suck up to the Trump base,

resulting in fewer Floridians being protected from a disease that is killing

literally hundreds of Americans every day. Using

rhetoric that feeds bigotry and hate against gay, lesbian, and trans people. Intimidating

the college board so they strip the Black Lives Matter movement out of their

advanced placement African-American Studies curriculum. Lying to

asylum-seekers to get them on a plane to Martha’s Vineyard as a stunt to

elevate his own political fortunes. Ron DeSantis is just fine with all of this. Cruelty is his

trademark. Ignoring

the health and safety of his state’s citizens, DeSantis led Florida into a

veritable Covid Armageddon, letting (as of January 16th) 84,176 of his citizens die from the disease.

As former FDA commissioner Dr. Scott Gottlieb told CBS’ Face

The Nation: “They

let the virus spread largely unchecked in terms of personal mitigation. People

weren't wearing masks. They weren't encouraged to wear masks. Vaccination was

encouraged for the elderly population, but not widely… So they made policy

choices, and the consequence was an infection that largely engulfed most parts

of the state.” After this

orgy of death and disease, at the end of 2021 about 12 percent of Florida’s

population — almost 2.6 million — still lacked any form of medical insurance

because of DeSantis’ refusal to expand Medicaid for low-income people. And now as

many as 2 million more Floridians will join the ranks of the uninsured in the

coming months. | |||||||||||||||||||||||||

This is today's Hartmann Report, published by Substack:

Hairdryer Climate Mathematics RevealedOur hairdryer math gets really bizarre when we apply it to global warming |

By THOM HARTMANN

Most

people know that a hairdryer draws about as much power as your average modern

outlet will give it — typically around 1000 watts or, at 110 volts, just shy of

10 amps. (Plug in and turn on two hairdryers from the same outlet and you’ll

usually blow a circuit breaker: most homes max out at 15 or 20 amp circuits.)

If those numbers are gibberish to you, hang on: it’ll all have

meaning in a moment, particularly when I get to the really shocking part about

climate change and hairdryers.

I was

recently listening to a rightwing radio talk show host trashing electric cars

and the need for them (he was also denying climate change) and he went into

this rant about how if everybody in America bought an electric car, charging

them would “take down the entire country’s power grid.”

This assertion

is, to be charitable, BS. But since we all know what a hairdryer is and have,

at least, a sense for how much power one typically uses — the equivalent of ten

100-watt light bulbs — let’s convert an electric car’s power usage into

hairdryers.

A typical

electric car using a 110 volt home charger pulls about the same amount of

electricity when it’s charging as does a hairdryer: between 800 and 1200 watts,

or 8 to 12 amps, with an average of 10 amps or around 1000 watts per hour (one

kilowatt-hour).

So, charging your car is about the same as running a hairdryer,

our new unit of measurement.

The

average electric car travels 100 miles on around 30 kilowatts

(30,000 watts or 30 “hairdryer-hours”) of electricity (Tesla Model 3 only uses

25, the Chevy Bolt 29), while the average driver in America travels around 1000 miles a month or 33 miles

a day: roughly 10 kilowatts or 10 hairdryer hours a day to cover those 33

miles.

So the

average driver charging their car overnight for ten hours (to replenish that 10

kilowatts of electricity to travel 33 miles) will use the same amount of

electricity as running a single hairdryer for 10 hours.

First off, you can see how silly it is to argue it would “take

down the grid” if every family in America were to turn on a single hairdryer in

their home for 10 hours every night, the equivalent of everybody recharging 33

miles worth of driving every day.

Particularly because most of that charging is done overnight,

when electric demand is lower than normal.

(The

average cost of electricity in the US, by the way, is $.10 per kilowatt hour, or ten cents per

“hairdryer hour.” So, simple math suggests it costs about $3 to drive 100 miles

— 30 “hairdryer hours” worth of electricity x 10 cents per hour — in the

average electric car. For comparison, in the average 25 mpg gas-powered car that same 100

miles would consume 4 gallons of gasoline, costing around $16 at four dollars a

gallon.)

But our hairdryer math gets really bizarre when we apply it to

global warming.

Our planet

isn’t warming because we’re all running hairdryers or even cars or home

furnaces; it’s warming because the greenhouse gasses we’re pouring into the

atmosphere from

generating electricity, heating our homes, and driving our gas-powered cars are

acting like a giant blanket, trapping heat from the sun in the atmosphere.

In other words, we are not warming the Earth (at least not

significantly) with the heat we’re adding: it’s the greenhouse gasses

(principally carbon dioxide) that are warming the Earth by trapping heat

from the sun that would otherwise radiate out into space.

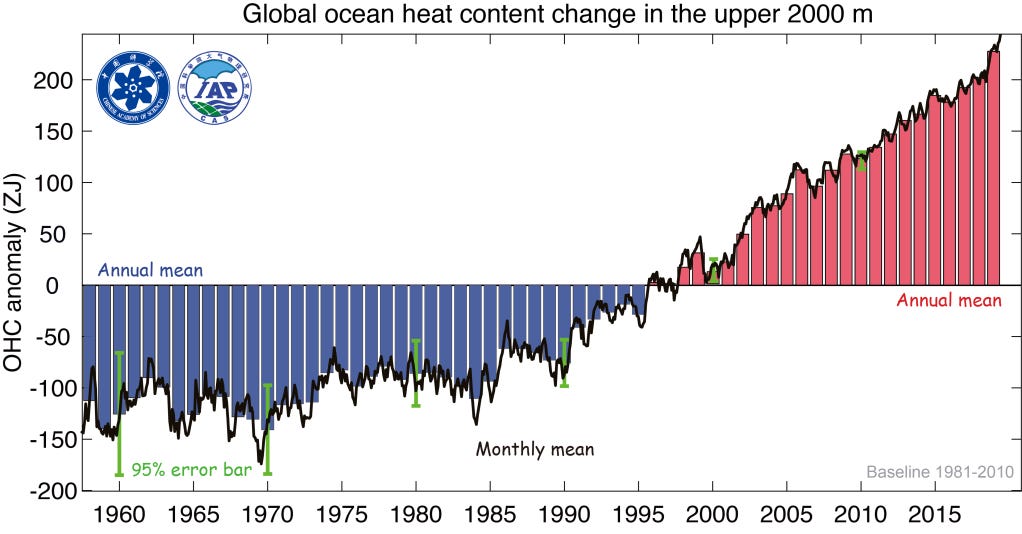

A new

study published this week in the journal Advances in Atmospheric Sciences

found that our oceans — which absorb about 90 percent of the increased heat in

the atmosphere from global warming — took in and held an absolutely massive

amount of solar energy last year.

As Damian Carrington, the Environment Editor at The Guardian,

put it in a recent article summarizing that

new study:

“The

oceans absorbed about 10 zettajoules more heat in 2022 than in 2021, equivalent

to every person on Earth running 40 hairdryers all day, every day.”

Clearly, all 8 billion of us aren’t anywhere close to

using the power equivalent of 40 hairdryers all day, every day. But that’s the

amount of extra energy our planet is trapping every year at our

current rate of energy consumption because greenhouse gasses are so very

efficient at trapping solar heat.

As a

result, our oceans are warming. And that’s driving “atmospheric rivers,”

derechos, “bomb cyclones,” and a whole variety of other atmospheric phenomenons

we’d never seen or even heard of before the past decade or two.

|

|

Again, it’s not our energy use that’s driving this. It’s the

carbon waste byproduct — mostly CO2 — of the fossil fuels we’re burning

to create that energy that’s doing most of it.

If we were

simply capturing all our energy from the sun and wind, that blanket of

greenhouse gasses wouldn’t keep growing, the heat wouldn’t continue

accumulating, and our atmosphere might stabilize (assuming — and it’s not a

safe assumption — that we haven’t already passed tipping points that can’t be

reversed).

By the

1970s it was common knowledge across the scientific community that these

greenhouse gasses — particularly CO2 and methane — were warming our planet. As

you can see from the graphic above, it became irrefutable by the 1990s.

In 1979 President Jimmy Carter pointed to this knowledge and

these trends and took action to try to stop the crisis the world is now

experiencing.

“The

energy crisis is real,” Carter told the nation. “It is worldwide. It is a

clear and present danger to our nation. These are facts and we simply must face

them.

“What I

have to say to you now about energy is simple and vitally important.

“Point

one: I am tonight setting a clear goal for the energy policy of the United

States. Beginning this moment, this nation will never use more foreign oil than

we did in 1977 -- never.”

He declared a national crisis that year and proposed legislation

to create:

“[T]his

nation’s first solar bank, which will help us achieve the crucial goal of 20

percent of our energy coming from solar power by the year 2000.”

Tragically

for America and the world, it all came crashing down 43 years ago this month

when the fossil fuel industry’s candidate, Ronald Reagan, replaced Carter,

killed the solar bank and the solar bond program, and even took Carter’s solar

panels off the roof of the White House.

Reagan embraced the fossil fuel industry with gusto (and they

embraced him back), promoting climate deniers like James Watt to head the

Department of the Interior (which oversees oil, gas, and coal drilling and

mining), and Neil Gorsuch’s mother, Anne Gorsuch, to head the EPA.

Simultaneously, the fossil fuel industry began throwing millions

of dollars a year into sellout scientists and climate deniers while pouring

billions around the world into politicians and political campaigns.

As a

result, we actually increased

our consumption of fossil fuels — and the fossil fuel industry made hundreds of

billions in profits. Our World in Data summarizes it well:

|

|

Electric

cars are a huge step forward because they don’t consume fossil fuels

(transportation is our second-largest producer of greenhouse gasses), but most

of our world’s electricity is still produced using coal, oil, or natural gas.

President Carter tried to save America — and lead the world away

— from the climate disasters that are killing millions of people around the

world every year. The fossil fuel industry and the Republican Party killed his

efforts here, as have “conservative” political parties and the fossil fuel

industry all around the world.

It’s

gotten too late to consider this anything other than a potential Armageddon.

We’ve

reached the crisis point where we can no longer afford anything even close to

business as usual. This is a climate emergency.

Yet here

in America the Republican Party continues to deny climate change and Republican

politicians do everything they can to block green and renewable fuels, all in

service to a grotesque industry that makes billions in profits every year from

killing our planet.

But we are

not without solutions.

Heating our houses and places of business, for example,

represents our biggest use of fossil fuels. Yet in Urbana Illinois, Vancouver Canada, and across Germany they’re building homes that are so

efficient they can be… wait for it… heated with a single hairdryer.

A new and

better world is possible,

if we can only overcome the money of the fossil fuel industry, the corruption

of a political party, and stop squandering the little remaining time we have

before, if we don’t act, climate disasters overwhelm civilization.

Here's the intro to the article - link to full article is below:

But that doesn’t mean you should feel helpless, or that your actions aren’t worthwhile. Taking steps to lower your own carbon footprint may help ease your climate anxiety by giving you back some power — and even the smallest of actions will contribute to keeping our planet habitable.

With that in mind, here are 10 places to start.

Every vote for Speaker of the House in which the Dems vote for their Democratic leader is a wasted vote.

Recognizing that they're not going to get a Democratic Speaker, they should nominate a Republican that as few as six Republicans would vote for. I suggest Liz Cheney or Adam Kinzinger, but there are others too!

There are enough Republicans, I'd guess, who are pissed off at those 19 far right members who are blocking Kevin McCarthy, that electing Liz Cheney or Adam Kinzinger might give them an opportunity to get revenge!

Here's an excerpt. You can subscribe to his daily email on Substack.

In most developed countries homelessness is not a crisis; nobody goes bankrupt because somebody in their family got sick; and jobs pay well enough and have union pensions so people can retire after 30 or 40 years in the workforce and live comfortably for the rest of their lives.

But not in America. Republican politicians have fought tooth-and-nail for generations to prevent any of those things from happening here.

Which raises the question: “Why?”

Why do Republican politicians promote hateful messages and cruel policies? Why are Republican-run states the real “shithole” parts of the US with the highest rates of poverty, violence, early death, disease, and illiteracy?

What motivates these Republican politicians to say they’re for the “little guy” when the only policies they pursue are to cut taxes on the rich, gut unions, destroy public schools, and ship jobs overseas?

It’s not about ideology.

Republicans don’t hate Social Security and Medicare, for example, because they’re afraid that those programs are going to somehow turn America into a “socialist” country. They hate those programs because they’re paid for with tax dollars, and greedy Republicans hate to pay their fair share of taxes.

It’s not about racism, although it often appears that way.

The reason Republicans work so hard to keep Black and Brown people down is because they subscribe to a weird economic theory that “requires” an underclass who do most of the hard work for very little money. Thus, morbidly rich Republican “donors” — being part of the overclass — can reap the benefits of increased corporate profits while keeping their taxes low so they can stuff the extra cash into their money bins.

If their use of racist language and Confederate iconography brings in a few more low-IQ white voters, that’s just icing on the cake. They can use the racist yahoos to get themselves reelected so giant corporations will continue to stuff their SuperPACs with lobbyist cash they can use for their own retirement.

It’s not about charity: they say that the housing and healthcare needs of poor people should be taken care of through “private philanthropy” instead of government.

What they’re really saying is that they don’t want to pay their fair share of taxes to maintain a healthy society. By cutting government support for poor and working-class people, as Anand Giridharadas documents so well, those very average Americans will become more dependent on the noble philanthropists among the billionaire class and less bonded to their own nation’s government.

It’s not about Christianity, although they’re constantly invoking Jesus for everything from pushing the death penalty on women who want to get an abortion to giving bigots the legal right to discriminate against gay, lesbian, and trans people.

Jesus never once mentioned abortion and decried bigotry, but they regularly ignore and even flout His teachings in the Sermon on the Mount and His warnings in Matthew 25. They protect multimillionaire evangelists’ tax-free status, and the preachers repay them by preaching politics from the pulpit.

It’s not about saving Americans from the pandemic or concern for public health.

Trump used the Defense Production Act, for example, to force mostly Brown and Black meatpackers back to work, not to keep Americans safe. As long as the factories are humming and the stock market is rising, a few hundred thousand dead Americans are just collateral damage.

It’s not about conservatism.

They’re not interested in slowly or “cautiously” improving society, or “conserving” anything other than the balances in their own checking accounts. They like to use the word “conservative,” but they’ve rendered it meaningless at best and code for “racist” at worst.

It’s not about making the world a better place.

Republican politicians deny climate change, deregulate industries that poison our air and water, and do everything they can to screw working people out of unions, good wages, and decent benefits. They’re totally down with pesticides that are killing our pollinators while they poison our atmosphere with their carbon emissions, all just to make a buck.

It’s not about having a better-educated electorate or populace.

They’ve spent decades trying to destroy our public education system that was, in the 1960s, the envy of the world. When they did away with free and low-cost college education during the Reagan years they kicked off almost $2 trillion worth of student debt which is preventing people from starting families, opening small businesses, or even buying their first house. But it sure is profitable for Republican-donor bankers!

It isn’t about “culture.”

They do a good-old-boy NASCAR/Duck Dynasty routine to bring in the rubes, but there’s no way Donald Trump would ever invite the average Republican voter with a giant flag and a pickup truck to any of his golf clubs, nor would Ted Cruz want to vacation with one of them or their families in Cancun.

It’s not about “gun violence.”

As long as their investments in weapons manufacturers are profitable and the problem of gun violence is limited to poor- and working-class Americans, Republican politicians don’t give a rat’s ass about “gun safety.” Although they’re happy to use guns as a wedge issue to bring in male voters who are insecure about their own masculinity.

It’s not about “protecting our children.”

The main through-story of the GOP attacks on queer people is that “they’re coming for your kids.” If Republican politicians actually cared about our kids, they’d do something about America being the only country in the world where gun violence is the leading cause of childhood death.

Republican politicians know that most pedophiles are straight men, but attacking defenseless minorities has been the cheap trick of craven demagogues from the eras of crusades, pogroms, and witch burnings to this day.

It’s not about immigrants taking jobs from working-class Americans.

After “reforming” our immigration laws in 1986, Ronald Reagan stopped enforcing the laws against wealthy white employers hiring people who are here without documentation (even though those employers were — and are — committing a crime by hiring undocumented workers).

As a result, entire industries like construction and meatpacking that once provided good union jobs have been de-unionized, their former American-citizen union employees replaced by low-wage workers without documentation.

And when the spotlight gets shined on those industries, Republicans are more than happy to put poor, hard-working Brown people in jail, but there’s no way they’re ever going to go after wealthy white employers. The Trump administration, for example, kicked off the midterm election year of 2018 by raiding over ninety 7-Eleven stores, hauling off undocumented Brown people for the cameras they invited to the arrests. Not a single employer went to jail, although they were the ones who initiated the “crime.”

Republican politicians don’t give a damn about your job, particularly when they can find somebody else to do it cheaper.

It’s not about putting America or Americans “first.”

Reagan and Bush the Elder negotiated NAFTA and revived the General Agreement on Tariffs and Trade (GATT) so businesses could offshore entire factories. Since the Reagan administration instituted neoliberalism in 1981, over 60,000 factories have left America, taking along with them at least 15 million jobs.

Donald Trump‘s rewrite of NAFTA even gave American companies a huge new tax break if they’d move their factories from America to Mexico.

At the end of the day, all Republican politicians care about is money. Greed is their principle animating force, and what binds them to their morbidly rich donors.

The greed embraced by Republican politicians — and the billionaires and CEOs who fund them — is why average Americans can’t have nice things. It’s why we and our children must walk the tightrope of life without the same safety net other countries — from Canada to Costa Rica, France to Taiwan — offer their citizens.

It doesn’t matter to Republican politicians how many Americans die unnecessarily, how many of our fellow citizens struggle in misery and poverty, how many children’s growth is stunted or bodies and brains are poisoned by industrial and mining waste being poured into our air and rivers.

As long as the money keeps rolling in and the GOP’s billionaire patrons keep paying less than 3 percent in income taxes, greed is all Republican politicians care about or are willing to fight for.